The term ‘working capital’ gets thrown around a lot, but what does it actually mean? Working capital measures a business’s ability to pay off its current liabilities with its current assets. It plays a large role in a company’s success and affects several aspects of a business, including funding inventory and planning for long-term growth.

To make sure your company’s working capital is up to par, it’s critical to understand what it means, how to calculate it, and why it’s important to the success of your business. In our guide, we cover all of the above, including when it’s OK to have negative working capital. Click here to jump to the infographic for a quick overview of working capital.

What is Working Capital?

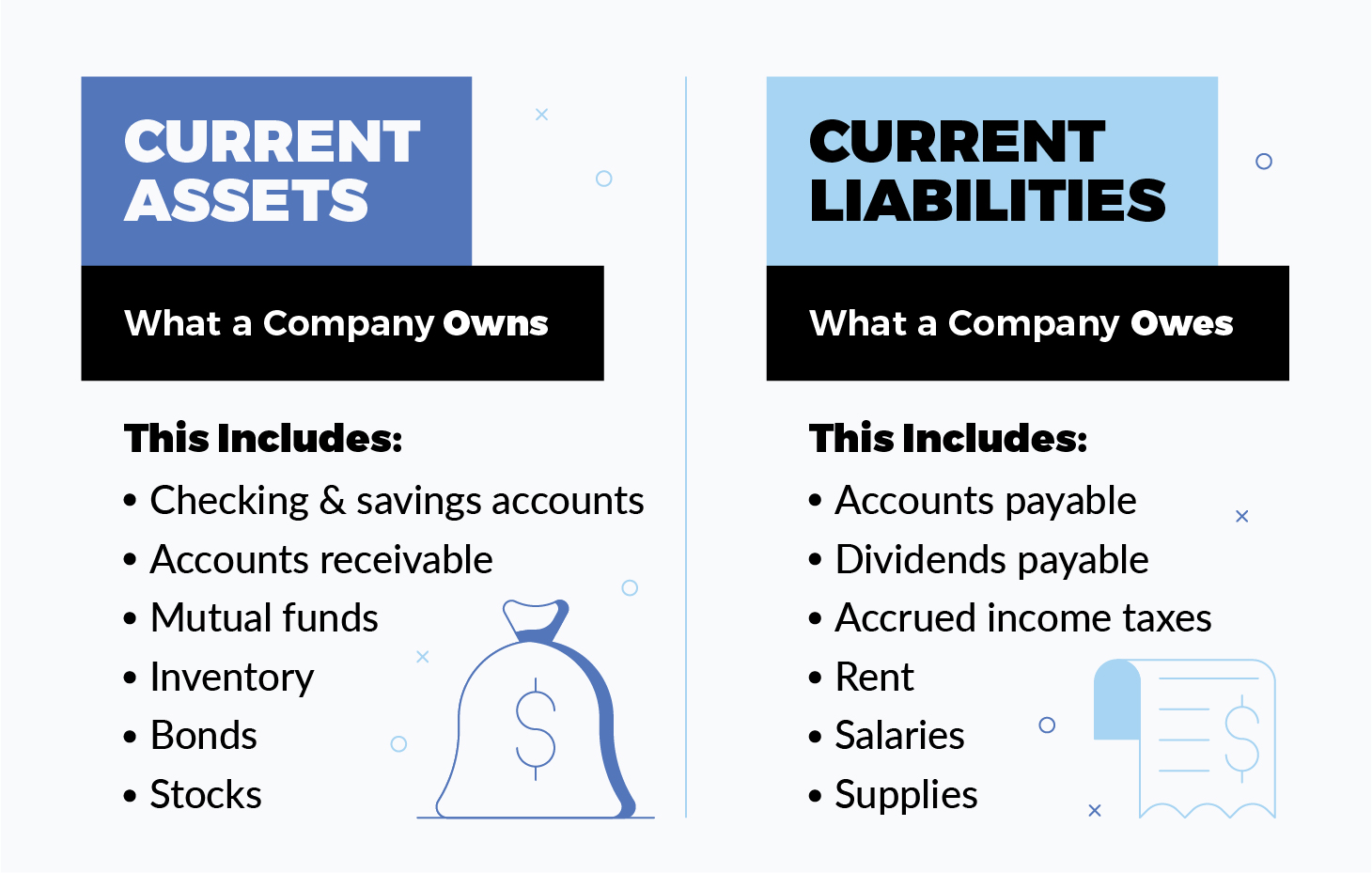

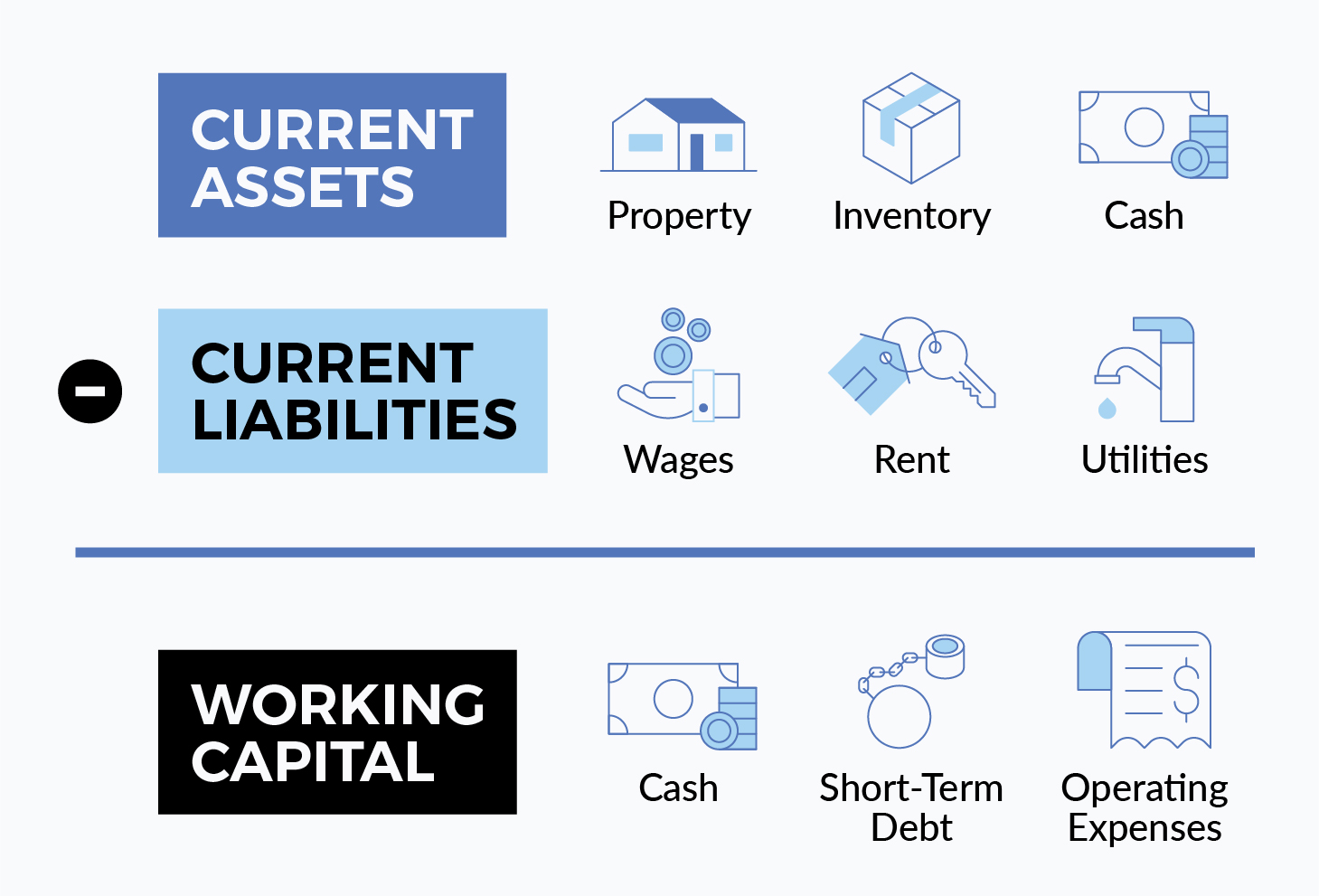

Working capital, also referred to as net working capital (NWC), is the difference between a company’s current assets (what the business owns) and current liabilities (what the business owes). It’s a way to measure a company’s short-term financial health, operational efficiency, and liquidity. Working capital tells creditors whether a company is able to pay off their debts in a year.  Current assets are tangible and intangible goods a company owns that can be turned into cash. This includes checking and savings accounts, accounts receivable, inventory, bonds, mutual funds, and stocks.

Current assets are tangible and intangible goods a company owns that can be turned into cash. This includes checking and savings accounts, accounts receivable, inventory, bonds, mutual funds, and stocks.

Current liabilities are any debts and expenses the company has incurred within a year (or one business cycle). This includes everything from rent, utilities, and supplies to accounts payable, accrued income taxes, salaries, and dividends payable.

When a company’s current assets exceed current liabilities, they have positive working capital. If a company has considerable positive working capital, then it has the potential to grow. When a company has the same amount of current assets and current liabilities, it is referred to as zero working capital. This is most prominent in demand-based organizations, where there is little to no inventory.

How Do You Calculate Working Capital?

The formula for calculating working capital is a company’s current assets minus its current liabilities. This measures short-term liquidity and the ability to pay off short-term debts within one year.

The formula for calculating working capital is a company’s current assets minus its current liabilities. This measures short-term liquidity and the ability to pay off short-term debts within one year.

Current Assets - Current Liabilities = Working Capital

Working capital can also be determined by finding the current ratio. The current ratio is a company’s current assets divided by its current liabilities.

Current Assets / Current Liabilities = Current Ratio

Here’s an example:

A commercial construction company has $450,000 in assets and $312,000 in liabilities.

450,000 / 312,000 = 1.44

The higher the ratio, the better. However, this number will depend on the industry average. Aim for a current ratio that is in line with the industry average or a little higher. While a lower ratio can indicate risk, a ratio way above the industry average can indicate irresponsible use of assets.

How Much Working Capital Does a Company Need?

The amount of working capital a business needs is subjective to the industry and type of business. Different types of businesses need different degrees of working capital to operate efficiently. However, a healthy business should have an ample amount of current assets to pay off current liabilities.

A higher ratio is a sign that a company is able to pay off its short-term liabilities and debt. It also means it can easily fund day-to-day operations. If a company is looking to invest and grow, they need to have positive working capital. A ratio greater than 1 means current assets exceed current liabilities. It also means a company can convert its assets into cash at a faster rate. According to divestopedia, “a buyer usually likes to see a working capital ratio of 1 to 1.5 times, which means there is at least one dollar of current assets for every dollar of current liabilities.”

However, the amount of working capital needed is subjective to the business. Companies that deal with large amounts of physical inventory, for example, often require more working capital to flourish. In short, you should always have enough working capital to meet any short-term financial obligations.

Reversely, having too much working capital can sometimes be a bad sign to investors. It could indicate that the business is not using its resources efficiently or is being too conservative with its finances. This happens when there are uncollected accounts receivable, funds are tied up in day-to-day operations, or there is a surplus of unsold inventory.

What is Negative Working Capital?

Negative working capital is when a company’s current liabilities are greater than its current assets. This results in a current ratio less than 1. This can happen when a business has a substantial increase in accounts payable as a result of a large purchase of services or products.

If a company’s working capital is negative for an extended period of time, this is a bad sign to investors and creditors that a company’s current assets are not being used efficiently. Negative working capital can result in a liquidity crisis and bankruptcy court if not handled immediately.  Depending on the business and industry, sometimes it is OK to have negative working capital. Businesses that can generate cash very quickly, such as grocery stores and fast-food chains, need little working capital to still do well. This is due to high inventory turnover rates. For example, grocery products bought from suppliers are quickly sold to customers before the grocery store has a chance to pay the supplier. The cash generated can be used to pay off accounts payable upfront.

Depending on the business and industry, sometimes it is OK to have negative working capital. Businesses that can generate cash very quickly, such as grocery stores and fast-food chains, need little working capital to still do well. This is due to high inventory turnover rates. For example, grocery products bought from suppliers are quickly sold to customers before the grocery store has a chance to pay the supplier. The cash generated can be used to pay off accounts payable upfront.

Companies that have substantial brand recognition can oftentimes be OK operating with negative working capital because they have public support and can easily raise funds. They also usually have great relationships with suppliers and are able to bargain for discounts. However, if working capital is negative for a long period of time, it can become a serious problem.

Reasons Your Business Might Need More Working Capital

While the needs of working capital vary by industry and business, some of the most common reasons a business might need more working capital are:

While the needs of working capital vary by industry and business, some of the most common reasons a business might need more working capital are:

- Short-term debt obligations: Paying off short-term liabilities, such as equipment needs, inventory purchases, and salaries are vital to daily operations. Working capital is needed to turn short-term assets into cash, fast.

- Applying for a surety bond: A surety considering a company for performance bonds and payment bonds will require a working capital position of 5 to 10% depending on the size of the contractor. For example, if a contractor is looking for $10,000,000 in total bond capacity, the surety would need to see $1,000,000 to $500,000 in working capital. Additionally, underwriters are more likely to offer discounts on surety bond costs when a company has sufficient working capital.

- Growth and expansion: If you’re a new business looking to grow or if you’re a seasoned business looking to expand into new markets, you need working capital to fund production. Negative cash flow can inhibit your chances of expansion.

- Emergency preparedness: Similar to personal finances, businesses want to have a healthy amount of cash tucked away in case of emergencies. Things like lawsuits, loss of customers and natural disasters can have a significant impact on budget. Make sure you have enough working capital available to handle any unexpected costs.

- Seasonal differences: If your business experiences seasonal differences, extra capital may be needed to prepare for a busy season. If you experience slow months, you’ll need positive working capital to ensure your company stays afloat.

- Attracting investors: Inadequate working capital can be a red flag to investors. Having sufficient working capital shows creditors and investors that the business has the ability to repay a loan.

How to Improve Your Working Capital

Working capital is key to ensuring the day-to-day operations of a business run smoothly. If you find yourself short of cash, working capital can be increased in a few ways:

- Improve accounts receivable: Encourage customers to pay on time by offering incentives.

- Pay debt on time: Avoid unnecessary penalties and use electronic payment systems to ensure all debt obligations are met on time.

- Take advantage of tax incentives: Tax incentives save money that can be used for working capital funds.

- Cut unnecessary expenses: Audit your monthly expenses and break it down into components. Is everything you're paying for necessary? Do you have signs of scope creep for a few projects? Trim the fat and focus on expenses that maintain company functionality.

- Avoid stockpiling: Manage your inventory so that every item is sold and products arrive exactly when you need them. When inventory is quickly converted to cash, less capital is tied up in unused assets.

- Working capital loans: If needed, working capital loans are available to fund short-term operational needs.

Working capital is important for businesses of all sizes and it should be monitored periodically. Efficiently managing working capital ensures a company is running smoothly. It can also increase a company’s earnings and profitability over time.

While you can’t predict every obstacle that comes your way, you can prepare. Having sufficient working capital available will ensure your business is covered in the event of a hardship. It can also give you insight into whether it’s time to expand or cut costs. For more information on working capital and why it’s important, check out the infographic below.

Leave a Reply