How Much Does a Surety Bond Cost?

Surety bond costs are typically 1-10% of the bond amount, but this varies by the bond type required of you and your financial strength.

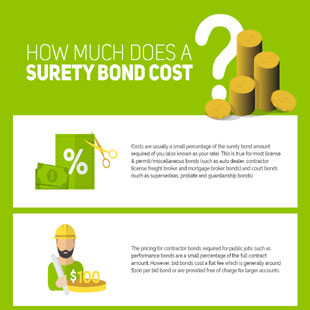

Generally speaking, the cost of a surety bond is calculated as a small percentage of the total bond amount that is required to be in place. Contractor bonds specific to public jobs, though, are based on the full contract amount.

Understanding Your Premium

Your premium is the percentage of the total bond amount that you need to pay, and it directly reflects how risky you seem to surety companies. This perceived risk can be influenced by factors such as:

- Your credit score

- Financial statements

- Owned assets

- Industry experience

- Your claim history

Rates vary based on the likelihood of you causing claims by not adhering to the obligations your bond guarantees. It's important to note that if you do cause bond claims, the surety company will initially cover them. However, the lower your likelihood of triggering claims on your bond, the lower your premium is likely to be.

How is The Cost of a Surety Bond Calculated?

The cost of your surety bond is calculated as a percentage of the bond amount. This percentage fluctuates based on the level of risk the surety perceives you to represent. Typically, it ranges from 1% to 10% of the bond amount.

Example

Let's say you need a $25,000 surety bond for your business. The rate, based on your credit history, business financial statements, and industry experience, is 1.5%. This means the cost of your surety bond would be $375, or 1.5% of the required bond amount.

If you have less-than-ideal credit or minimal experience in your industry, your rate might be higher. For the same $25,000 bond, if the rate is 5%, the cost of your bond would be $1,250. This higher premium reflects the increased risk you pose to the surety.

What Factors Drive Surety Bond Cost?

This is a question we're often asked. The percentage of the total bond amount you pay is based on a handful of factors, including your credit score, the type of bond you need, your financial statements, verification of assets, and your experience in the industry. Let’s take a closer look at each.

Credit Score: Standard Market vs. Bad Credit

If you have good credit, meaning minimal or no negative marks on your credit report and a relatively high credit score, you are considered a standard risk to a surety agency. The price of your bond is calculated at a lower rate, so the percentage you pay is lower. With bad credit, the percentage of the total bond amount you pay will be higher because of this increased risk. See “Bad Credit Surety Bonds” for more information and FAQs.

Type of Bond

The type of bond you need will dictate how much you pay.

Freight brokers, for instance, are required to have a bond of at least $75,000 in place. Other bonds required by the Federal Government may also have higher bond requirements.

The higher the bond amount, the higher the cost to you since bond costs are calculated on the bond amount.

Financial Statements

Depending on your industry, financial statements may also be evaluated when you apply for a bond.

If you have weak financial statements or are unable to provide them, you are assumed to be a higher risk and therefore, pay a higher percentage of the bond total.

Asset Verification

Verifying the assets you or the business own is helpful in determining the risk you present as a bondholder. If you have no assets, and a negative credit history, you are likely to pay more for your surety bond than those who can verify their assets.

Experience in the Industry

Many of our clients find that their experience level influences their surety bond costs. Those who have been working in the same industry for several years and have few or no bond claims are considered much lower risks to surety agencies than those who are just getting started.

This principle was clearly demonstrated when we worked with Ted’s construction company. As a seasoned player in the industry with a record of no claims, Ted had built a strong reputation and shown significant growth. However, when Ted’s construction company first came to us, we noticed its unique profile: a strong industry reputation and significant growth, yet with financial statements that did not follow the traditional trajectory. This situation is quite common in the industry, and many of our clients face similar challenges.

Our team at JW Surety Bonds conducted a thorough assessment of Ted’s company. We considered Ted's extensive industry experience, his company's solid track record on previous projects, and the robustness of their ongoing contracts. However, we also had to balance these factors against their unconventional financial statements and relatively short history.

Traditionally, such a profile might lead to a higher surety bond premium due to perceived risks. But we believed in the company’s potential and Ted's expertise. By highlighting the company’s strengths and potential for continued success, we were able to offer them a very competitive rate.

Surety Bond Cost Infographic Guide

Surety Bond Costs by Bond Type

Several different types of surety bonds exist, and each requires a surety agency to look at your personal credit, financial statements and assets, and your experience in the business.

However, the type of bond you need also plays a role in the rate you pay for your bond. Here are several common types of bonds and some insight into how much they cost.

How Much Does a License Surety Bond Cost?

The cost of your license bond is based on the bond amount required by your city or state, the type of specific license you are seeking, and the other factors mentioned above.

Typically, this bond cost is between 1% to 10% of the total bond amount required for your license.

How Much Do Construction Bonds Cost?

The cost of a construction bond varies greatly depending on the specific type of bond you need. In most cases, however, the amount you pay is the same percentage range as other bonds, between 1% and 3% of the bond amount.

You can read our in-depth guide to determine what a performance bond costs. Also, we have put together information specific to bid bonds as well.

How Much Does a Fidelity Bond Cost?

The total cost you pay for fidelity bonds is based on the type of coverage you need, the amount of the bond, the number of employees you have, and certain controls you have in place for your business.

If you want to get a firm quote on your fidelity bond cost, you will need to fill out an application. You can also read our guide on how to get bonded and insured to get a better understanding of the costs associated with fidelity bonds and other surety bonds you may need.

How Much Does a Court Bond Cost?

All court bonds cost a percentage of the total bond amount, but the percentage you pay varies depending on the type of court bond you need.

- Probate bond costs are based mostly on personal credit, but pricing can also be impacted by other circumstances, like the complexity of the estate.

- Appeal bond costs are calculated using your business financial strength.

- Guardianship bond costs are dependent on personal credit score as well as the character of the applicant.

Surety Bond Cost Table

If you're looking for an estimated bond rate based on your credit score, the table below shows yearly premiums based on various credit rankings and bond amounts. Keep in mind this is just an estimate and does not take into account any taxes or extended bond terms.

| Surety Bond Amount | Yearly Premium | ||

|---|---|---|---|

| Excellent Credit (675 and above) |

Average Credit (600-675) |

Bad Credit (599 and below) |

|

| $5,000 Surety Bond | $50 - $150 | $150 - $250 | $250 - $500 |

| $10,000 Surety Bond | $100 - $300 | $300 - $500 | $500 - $1,000 |

| $15,000 Surety Bond | $150 - $450 | $450 - $750 | $750 - $1,500 |

| $20,000 Surety Bond | $200 - $600 | $600 - $1,000 | $1,000 - $2,000 |

| $25,000 Surety Bond | $250 - $750 | $750 - $1,250 | $1,250 - $2,500 |

| $30,000 Surety Bond | $300 - $900 | $900 - $1,500 | $1,500 - $3,000 |

| $35,000 Surety Bond | $350 - $1,050 | $1,050 - $1,750 | $1,750 - $3,500 |

| $40,000 Surety Bond | $400 - $1,200 | $1,200 - $2,000 | $2,000 - $4,000 |

| $50,000 Surety Bond | $500 - $1,500 | $1,500 - $2,500 | $2,500 - $5,000 |

| $75,000 Surety Bond | $750 - $2,250 | $2,250 - $3,750 | $3,750 - $7,500 |

| $100,000 Surety Bond | $1,000 - $3,000 | $3,000 - $5,000 | $5,000 - $10,000 |

| $1,000,000 Surety Bond | $10,000 - $30,000 | $30,000 - $50,000 | $50,000 - $100,000 |

For the most accurate bond quote, check out our instant online bond estimator.