The freight brokerage sector is facing the most turbulent bonding environment in more than a decade, with more than 5,400 brokers shutting down since 2022. But in my view, the Excess Bond Program isn’t a broad solution to this volatility—it's a niche tool valuable only for strong, established brokers working with large carriers that require additional protection.

Today, tightening credit standards, a historic wave of broker closures, rising fraud, and increased FMCSA scrutiny have reshaped how sureties approach freight broker bonds—and brokers are feeling the pressure.

At a time when margins are thin and carrier relationships matter more than ever, access to the right bonding solutions can determine whether a broker stays competitive, especially when working with high-volume shippers who require additional financial protections.

But unlike required federal BMC-84 and BMC-85 financial responsibility filings, the Excess Bond Program is not widely used nor universally necessary. Instead, it has emerged as a specialized tool for a narrow segment of strong, established brokers who serve large carriers with their own bond requirements. In today’s volatile market, understanding where excess bonds fit—and how broader underwriting dynamics are shifting—is essential for any broker preparing for 2026.

Why the Excess Bond Program Matters—Even If It’s Not Mainstream

While the Excess Bond Program is sometimes portrayed as a lifeline for strained brokers, the reality is more nuanced: the $25,000 excess bond is not a widely sought-after product. It isn’t required by FMCSA, and most brokers don’t need it to operate.

However, large national carriers—including companies like Albertsons, which maintain an independent $75,000 exclusive bond—use these additional bonds to protect their specific freight interests. For brokers pursuing contracts with these high-volume shippers, an excess bond may be mandatory.

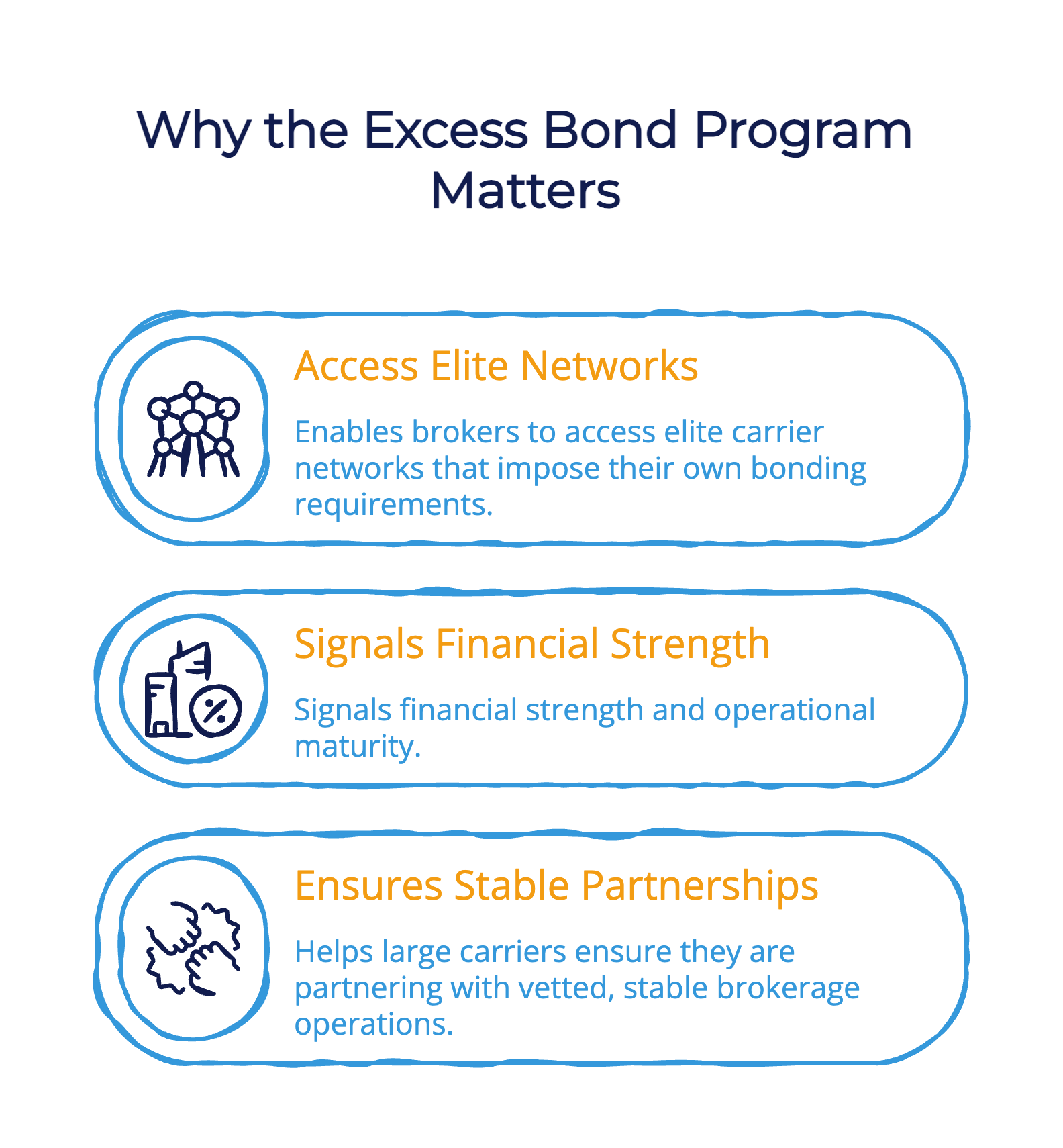

In those cases, the Excess Bond Program becomes a strategic tool:

- It enables brokers to access elite carrier networks that impose their own bonding requirements.

- It signals financial strength and operational maturity.

- It helps large carriers ensure they are partnering with vetted, stable brokerage operations.

But it is not accessible to everyone: new entrants, small brokers, and firms with credit challenges rarely qualify. Sureties restrict excess bond eligibility to brokers with strong financials, proven experience, and clean operating histories—criteria that have only tightened in the past two years.

In my view, brokers should treat excess bonds as a strategic tool—not a default step in their growth plan. If your book of business includes large carriers with supplemental bonding requirements, prepare early by strengthening liquidity and financial reporting. But if you’re not targeting those markets, avoid pursuing additional bond capacity just because it “feels” like the next level. Excess bonds provide value only when your operational strategy justifies them.

Who Actually Benefits From Excess Bonds Today?

New entrants and smaller firms will not qualify for an excess $25K bond nor the private bond mentioned above. Only strong freight brokers with qualified financial statements would qualify. This means that, in today’s environment, only well-capitalized, experienced brokers typically meet the underwriting thresholds.

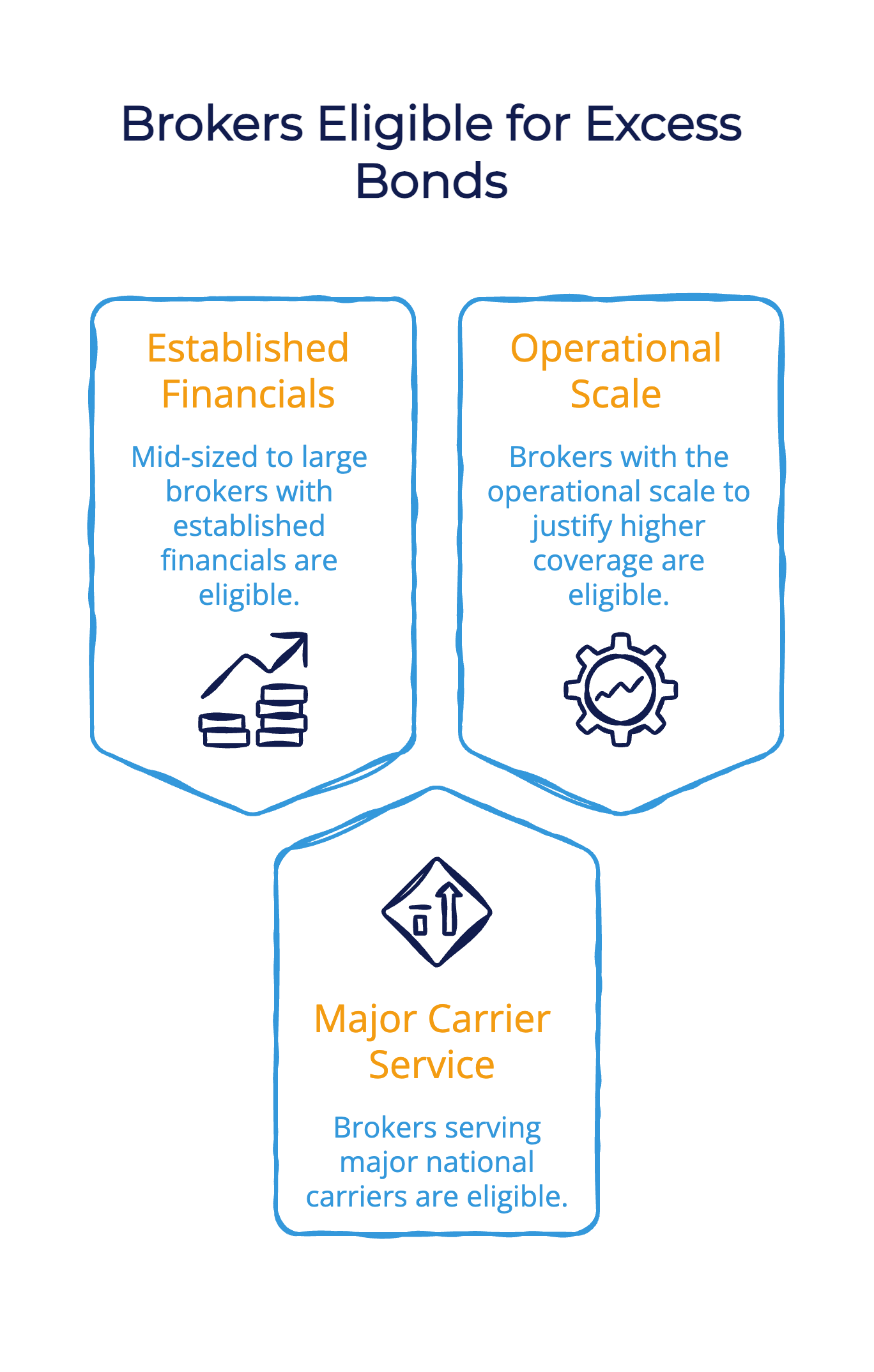

The brokers who benefit most are:

1. Mid-sized to large brokers with established financials

These firms can demonstrate liquidity, low debt utilization, and years of operational experience.

2. Brokers serving major national carriers

Large shippers sometimes require private bonds above the federal minimum. Without an excess bond, access to these opportunities disappears.

3. Brokers with the operational scale to justify higher coverage

Excess bonds signal reliability to carriers who move sensitive, high-value, or high-volume freight.

In contrast, startups and smaller brokers are almost universally declined. This is not due to lack of opportunity, but because sureties have drastically tightened appetite following steep industry losses and widespread fraud.

It’s clear to me that smaller and newer brokers should avoid fixating on excess bond capacity and instead focus on building financial strength through disciplined growth, sound credit management, and conservative overhead. When your financials tell the right story, sureties will be far more willing to increase your access to specialized bond products. Trying to jump ahead too early usually results in frustration—and wasted time.

A Tightening Freight Market Has Reshaped Surety Appetite

Following unprecedented claims activity in 2023 and 2024, the surety market for freight broker bonds contracted sharply. There were approximately 12 carriers previously. Now there are 5 active in the space.

The carriers that are willing to entertain this bond have increased premium pricing and increased standards of underwriting. This has significantly reduced choice to the consumer. But until fraud is eradicated from transportation, and profit margins improve for freight brokers, I think the same surety environment will continue into 2026 and possibly 2027.

Why? Because the combination of broker failures, widespread double brokering, identity fraud, and abuse of the claim process has made this one of the most loss-intensive commercial surety products in the U.S.

Sureties are reacting in three major ways:

1. Higher Premiums and Stricter Underwriting

Rates are rising, credit minimums are tightening, and many carriers no longer accept brand-new brokers.

2. Limited Carrier Choice for Brokers

With fewer sureties in the space, brokers have less leverage, fewer quotes, and more rigid requirements.

3. Longer Review Cycles and More Verification

Sureties are investing in identity verification and fraud prevention to combat false filings and stolen identities.

This environment is expected to continue through 2026—and likely into 2027. Until fraud declines and broker profitability rises, surety capacity will remain constrained.

Given what I’m seeing industry-wide, brokers should be preparing for a multi-year period of constrained surety capacity. The brokers who maintain strong books, communicate proactively, and resolve financial or credit weaknesses ahead of renewal will secure better pricing and more stable carrier relationships. Sureties are prioritizing dependable, disciplined accounts—and the gap between preferred and marginal risks is widening.

Claims Are Up—But Actual Losses Are a Different Story

Surety companies need to have a robust claims department when writing these bonds. Only 1 out of 10 claims that come in on a freight broker actually get paid out as a loss, however, nuisance claims are a real issue..

Since the companies are required by law to review and investigate each claim and respond to the claimant, even in the event of no paid loss, the claims administration expense to the surety is huge. Thousands of nuisance claims—often duplicate filings, billing disputes, or submissions from parties with no valid contract—are submitted every day.

Each one requires:

- Legal review

- Investigation

- Formal written response

Even when no payment is made, administrative costs run into the millions, forcing carriers to raise premiums and tighten eligibility. This claims burden is a major driver behind today’s reduced surety appetite.

To put it plainly, brokers that treat documentation and communication as non-negotiable business practices fare dramatically better in the long run. Clear agreements, strong recordkeeping, and proactive dispute resolution prevent many claims from ever reaching a surety’s desk. The fewer frivolous claims attached to your MC number, the easier it is to maintain favorable pricing and underwriting support.

What Underwriters Are Looking for Now (That They Didn’t Five Years Ago)

Thanks, in part, to In part, to a wave of bankruptcies over the past year, with a total of 21 in the third quarter of 2025 alone, and a high incidence of fraud, there are a number of things surety carriers look at now more closely.

Years of experience is a big one, and while personal credit is closely reviewed, bond terms are not provided just based on credit score. Sureties will look at how much credit is in utilization (access to additional credit which is unused), if they own real estate (this is also a big plus point) and lastly, surety companies will require government issued identification to ensure we are talking to the actual person applying for the bond and that they will be running the business.

Key red flags include:

1. Limited Industry Experience

New brokers face the strictest scrutiny, and the number of years in business matters more than ever.

2. High Debt Utilization

Credit score alone is not enough. Underwriters closely analyze open credit availability and debt-to-income ratios.

3. Lack of Tangible Assets or Real Estate

Ownership of real property strengthens underwriting confidence.

4. Identity Verification Concerns

Due to rampant fraud, sureties now require government-issued ID and may perform digital identity checks.

From where I’m standing, brokers should see these trends as a roadmap for building a resilient operation rather than as obstacles. When you strengthen liquidity, adopt secure identity protocols, and maintain accurate financials, you’re not just meeting underwriting criteria—you’re building a brokerage capable of navigating market volatility and earning long-term trust from carriers and customers.

FMCSA Regulatory Shifts Will Transform the Landscape in 2026

The biggest change on the horizon is the FMCSA overhaul of the BMC-85 Trust Fund alternative. This will redefine who can act as a trustee and state that assets posted need to be liquid as opposed to the past 15 years where very little or no liquid assets were being pledged.

However, the FMCSA is also working on their own identity verification using face ID to ensure that the freight broker signing up to get an MC number and act as a freight broker is actually a real person!

Effective January 16, 2026:

- Only legitimate banks may act as trustees.

- Assets must be fully liquid, eliminating the past practice of accepting illiquid or improperly structured collateral.

This will effectively reduce BMC-85 usage to single-digit market share, closing a loophole that has contributed to fraud and broker instability for more than 15 years.

Additionally, FMCSA is developing:

- Face-ID identity verification for MC number applicants

- Potential citizenship requirements for new brokers

Looking ahead, any broker on a BMC-85 should begin evaluating alternatives now—well before trustee restrictions tighten. Transitioning to a BMC-84 may become unavoidable for many brokers, and preparing early will prevent operational disruption. Identity verification will also become mandatory, so building legitimate, traceable processes today will make compliance far easier once the rules shift.

Final Recommendation for Brokers in 2026

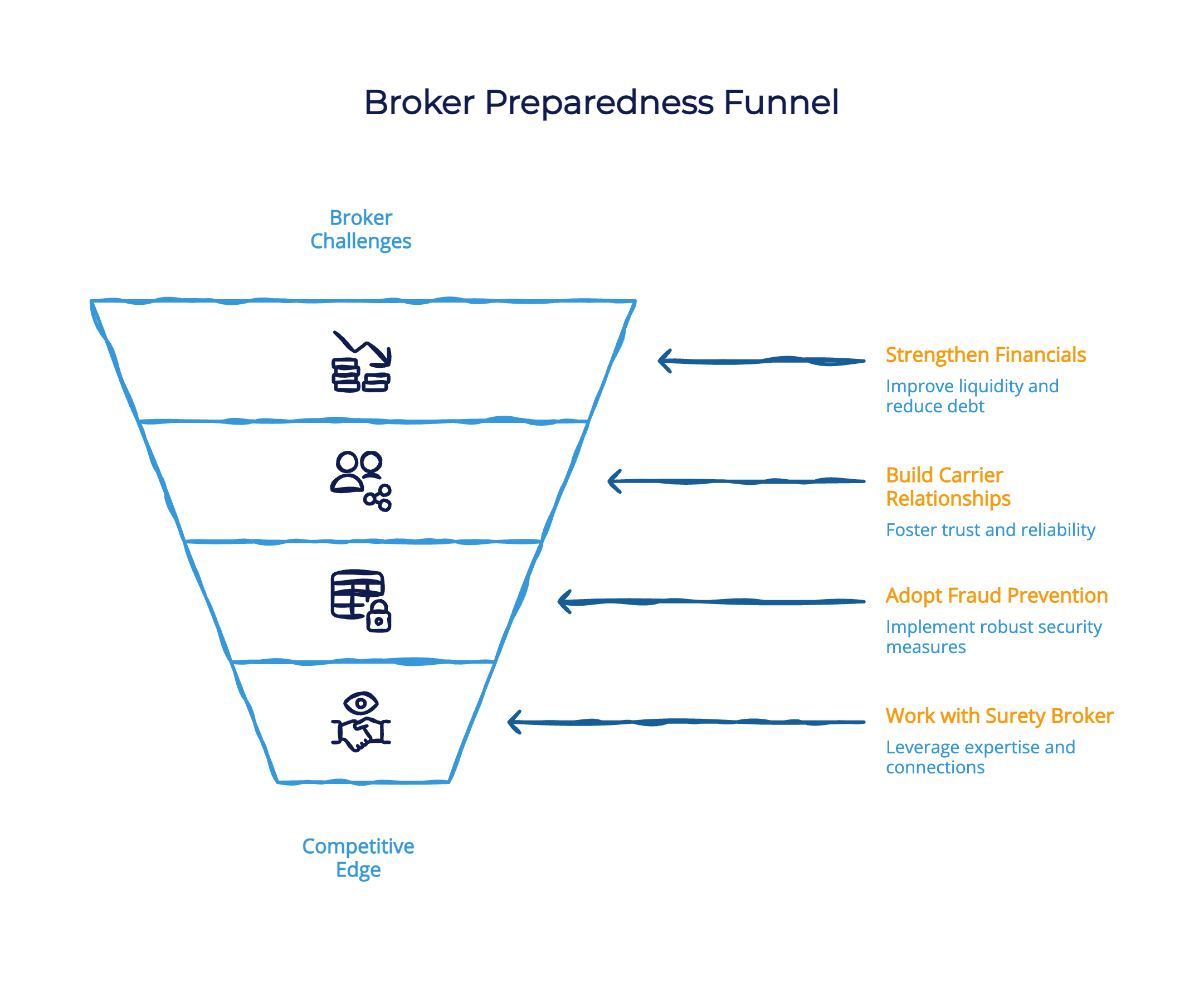

While the Excess Bond Program is not widely applicable, the broader bond market is evolving quickly. The freight market is undergoing a structural reshaping, and bonds are at the center of it. With fewer surety carriers, higher scrutiny, and new FMCSA regulations approaching, brokers must prepare early and proactively.To remain competitive, brokers should focus on:

1. Strengthening Financial Statements

Liquidity, low debt, and clean financials directly improve bond eligibility.

2. Building Strong Carrier Relationships

In a tight market, reliable brokers with good reputations are favored by both shippers and sureties.

3. Adopting Fraud-Prevention Processes

Use identity verification tools, secure carrier packets, and clear recordkeeping to avoid claims disputes.

4. Working with an Experienced Surety Broker

As capacity tightens, your broker’s relationships become a competitive edge.

My advice is simple: financial preparedness is your competitive edge. Strengthen liquidity, maintain accurate books, build trust with your surety partners early. Those who prepare before the 2026 changes land will be positioned to grow while others are still scrambling to adapt.

In a market defined by tighter underwriting, rising fraud exposure, and major regulatory shifts ahead, the brokers who will thrive are the ones who stay financially disciplined and build strong, transparent relationships with their surety partners. Strengthen your liquidity, maintain credible financials, and take a proactive approach to compliance long before 2026 arrives. That’s the standard we operate by at JW Surety.

Leave a Reply